SPONSORED CONTENT

Looking to provide health care coverage

designed for affordability?

There’s a solution available for small business owners in Florida

BY UNITED HEALTHCARE

With the current health care landscape bringing rising

administrative and premium costs, as well as increased

health care regulations, small business owners are

dealing with the financial challenges of offering adequate,

affordable coverage to their employees.

ALTERNATE FUNDING PLANS OFFER A WAY TO

CONTROL COSTS

Also called level-funded plans, alternate funding plans can help

small businesses reduce their overall health care costs and help

employees get more out of their benefits. These plans include

three components:

1. The employer’s self-funded medical plan. This pays medical

expenses for covered employees and their dependents.

2. A third-party claims administration agreement. The employer

enters into an agreement with the administrator, who provides

claims processing, billing, customer service and other services.

3. A stop-loss insurance policy. This provides coverage for large,

catastrophic claims by a single covered individual and provides

over-all coverage in the event all claims go beyond a certain

dollar limit.

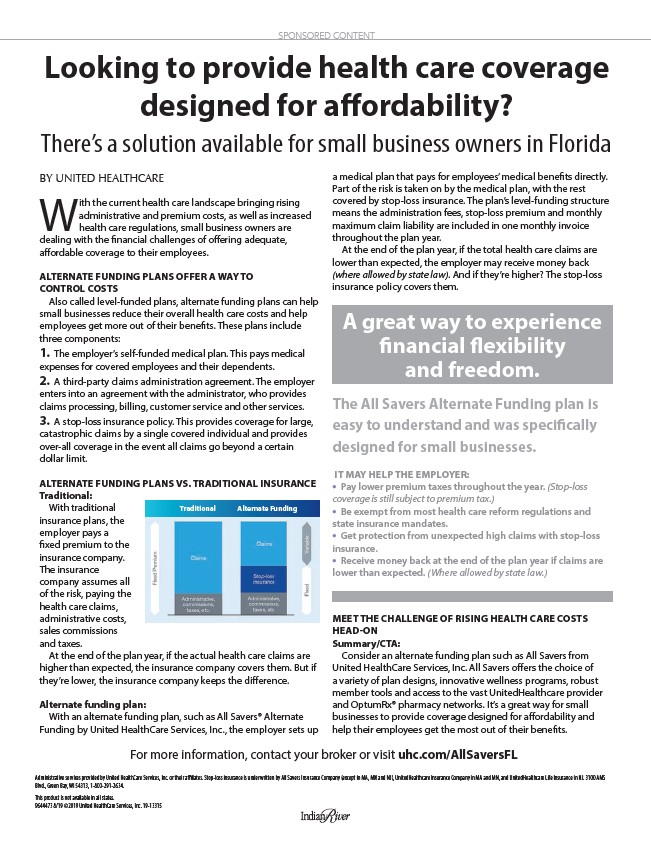

ALTERNATE FUNDING PLANS VS. TRADITIONAL INSURANCE

Traditional:

With traditional

insurance plans, the

employer pays a

fixed premium to the

insurance company.

The insurance

company assumes all

of the risk, paying the

health care claims,

administrative costs,

sales commissions

and taxes.

At the end of the plan year, if the actual health care claims are

higher than expected, the insurance company covers them. But if

they’re lower, the insurance company keeps the difference.

Alternate funding plan:

With an alternate funding plan, such as All Savers® Alternate

Funding by United HealthCare Services, Inc., the employer sets up

a medical plan that pays for employees’ medical benefits directly.

Part of the risk is taken on by the medical plan, with the rest

covered by stop-loss insurance. The plan’s level-funding structure

means the administration fees, stop-loss premium and monthly

maximum claim liability are included in one monthly invoice

throughout the plan year.

At the end of the plan year, if the total health care claims are

lower than expected, the employer may receive money back

(where allowed by state law). And if they’re higher? The stop-loss

insurance policy covers them.

Traditional Alternate Funding

A great way to experience

financial flexibility

and freedom.

The All Savers Alternate Funding plan is

easy to understand and was specifically

designed for small businesses.

IT MAY HELP THE EMPLOYER:

• Pay lower premium taxes throughout the year. (Stop-loss

coverage is still subject to premium tax.)

• Be exempt from most health care reform regulations and

state insurance mandates.

• Get protection from unexpected high claims with stop-loss

insurance.

• Receive money back at the end of the plan year if claims are

lower than expected. (Where allowed by state law.)

MEET THE CHALLENGE OF RISING HEALTH CARE COSTS

HEAD-ON

Summary/CTA:

Consider an alternate funding plan such as All Savers from

United HealthCare Services, Inc. All Savers offers the choice of

a variety of plan designs, innovative wellness programs, robust

member tools and access to the vast UnitedHealthcare provider

and OptumRx® pharmacy networks. It’s a great way for small

businesses to provide coverage designed for affordability and

help their employees get the most out of their benefits.

For more information, contact your broker or visit uhc.com/AllSaversFL

Administrative services provided by United HealthCare Services, Inc. or their affiliates. Stop-loss insurance is underwritten by All Savers Insurance Company (except in MA, MN and NJ), UnitedHealthcare Insurance Company in MA and MN, and UnitedHealthcare Life Insurance in NJ. 3100 AMS

Blvd., Green Bay, WI 54313, 1-800-291-2634.

This product is not available in all states.

9644473 8/19 ©2019 United HealthCare Services, Inc. 19-13315

/AllSaversFL

/AllSaversFL